Basis Adjusted MXN curve is used to forecast forward points and calculate Discount factors for each payment date.

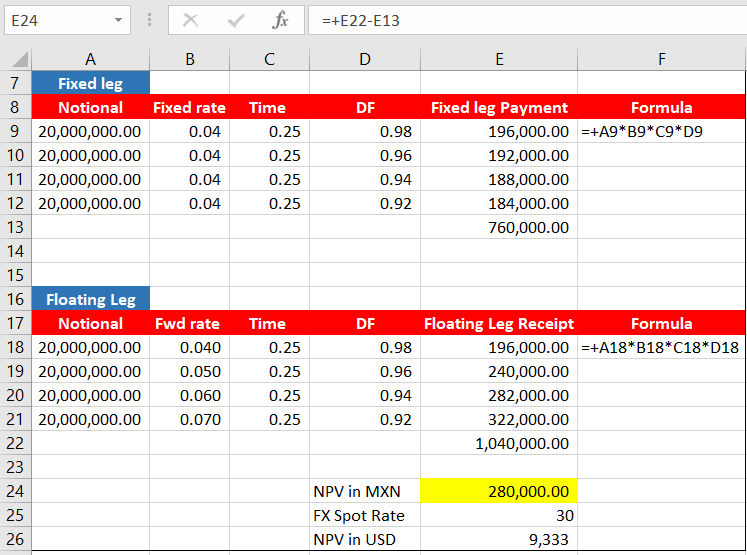

NPV = Floating Leg PV – Fixed Leg NPV

Leg PV = Notional * Fixed/Floating forward point * Time * DF

Quant library:

Basis Adjusted MXN Curve is calibrated using Zero and Basis curves. This is complex process. The final calibrated curve is used to determine forward points and discount factors for each fixed and floating leg.

Time is also determined by the quant library to exact calculation using Daycount basis, Holiday Schedule and Roll forward conventions.

SWAP RISK

MXN Zero(Base) Curve – PV01 is risk for one basis point on each bucket of the Zero interest rate curve.

MXN Cross Currency Basis Adjusted Curve – PV01 is risk for one basis point on each bucket of the Basis adjusted interest rate curve.

MXN Spot FX Rate – FX Delta risk (280,000 MXN pesos)